Your savings account is earning you almost nothing. While banks pay you 0.4% on your deposits, they lend that same money out at 7-8% interest. A CD (Certificate of Deposit) lets you earn the higher rate instead.

In this guide, we'll explain what CDs are, how the interest formula works, and how to use a CD calculator to maximize your returns in 2026. Whether you're saving for a short-term goal or looking for a safe place to park your emergency fund, understanding CDs can help you earn significantly more than a traditional savings account.

What Is a CD?

A Certificate of Deposit (CD) is a savings product where you agree to leave your money in the bank for a fixed period (the "term") in exchange for a higher interest rate than a regular savings account. CDs are offered by banks, credit unions, and online financial institutions. They are one of the safest investment options available because they are FDIC-insured (or NCUA-insured at credit unions) up to $250,000 per depositor.

Key Features of CDs

- Fixed interest rate — Your rate is locked in for the entire term, protecting you from rate drops

- Fixed term — Money is locked for 3 months to 5+ years depending on the CD type

- FDIC insured — Protected up to $250,000 per depositor, per bank

- Early withdrawal penalty — You pay a fee if you need money before maturity (typically 3-12 months of interest)

- Minimum deposit — Most banks require $500-$1,000 to open a CD

- Auto-renewal — Most CDs auto-renew at maturity unless you specify otherwise

Types of CDs

Not all CDs are the same. Here are the most common types you'll encounter:

- Traditional CD — The standard option. Fixed rate, fixed term, early withdrawal penalty.

- No-Penalty CD — Allows you to withdraw early without penalty. Usually offers a slightly lower rate.

- Bump-Rate CD — Gives you the option to "bump" your rate once during the term if rates rise.

- Step-Up CD — The rate automatically increases at predetermined intervals during the term.

- Jumbo CD — Requires a large deposit (typically $100,000+) but offers higher rates.

- IRA CD — A CD held within an Individual Retirement Account, offering tax advantages.

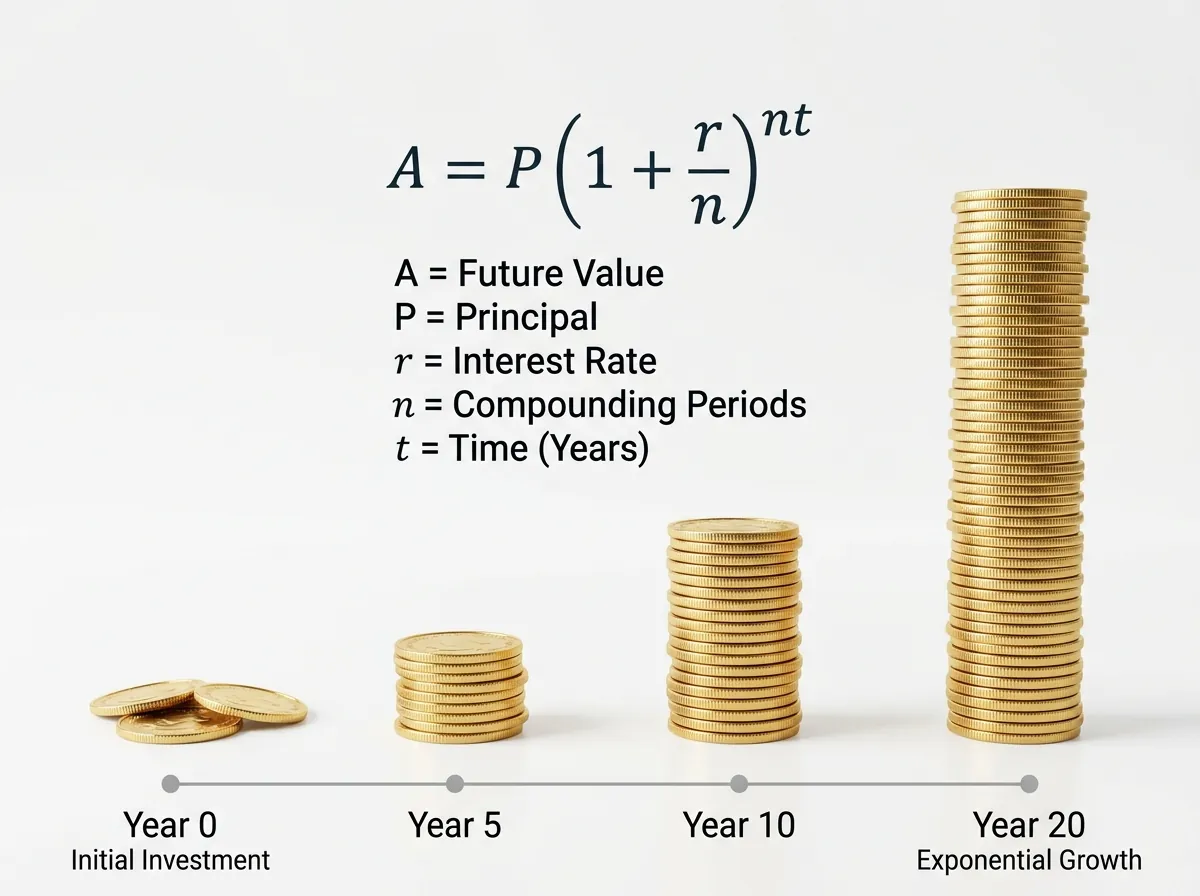

How CD Interest Works

CDs earn compound interest, meaning you earn interest on your interest. Unlike simple interest where you only earn on the original principal, compound interest calculates interest on both the principal and the accumulated interest from previous periods. This is why CDs grow faster than regular savings accounts.

The compound interest formula for CDs is:

Where: P = Principal (initial deposit), r = Annual interest rate (decimal), n = Compounding frequency (times per year), t = Time in years

Let's break down each variable:

- P (Principal) — This is the amount you initially deposit into the CD. For example, $10,000.

- r (Rate) — The annual interest rate as a decimal. For 4.5%, r = 0.045.

- n (Compounding Frequency) — How many times per year interest is calculated and added. Monthly = 12, Daily = 365, Quarterly = 4.

- t (Time) — The number of years your money is invested. For 12 months, t = 1. For 24 months, t = 2.

Example: $10,000 CD at 4.5% for 1 Year

| Compounding | Interest Earned | Final Value | APY |

|---|---|---|---|

| Annually | $450.00 | $10,450.00 | 4.50% |

| Quarterly | $457.65 | $10,457.65 | 4.58% |

| Monthly | $459.40 | $10,459.40 | 4.59% |

| Daily | $460.25 | $10,460.25 | 4.60% |

More frequent compounding means slightly more interest, but the difference between monthly and daily is only about $1 per year on a $10,000 CD.

CD vs Savings Account: The Numbers

| Feature | Savings Account | 1-Year CD |

|---|---|---|

| APY (2026 avg) | 0.4% – 0.6% | 4.75% – 5.10% |

| $10,000 earns in 1 year | $40 – $60 | $475 – $510 |

| $10,000 earns in 5 years | $200 – $300 | $2,500 – $2,800 |

| Liquidity | Instant access | Locked for term |

| Rate guarantee | Variable, can change | Fixed for term |

| FDIC insured | Yes (up to $250K) | Yes (up to $250K) |

A 1-year CD earns 8-10× more than a savings account. Over 5 years, that difference grows to $2,300+ on a $10,000 deposit.

When to Choose a Savings Account

Savings accounts are better when you need:

- Emergency fund access — Keep 3-6 months of expenses in a savings account for unexpected costs

- Short-term goals — Money needed within 3-6 months should stay liquid

- Regular deposits — If you're building savings gradually, a savings account allows ongoing contributions

- Flexibility — No penalties for withdrawals, no lock-up period

When to Choose a CD

CDs are better when you:

- Have a lump sum — If you have $5,000+ sitting in savings, a CD can earn much more

- Won't need the money — If you can lock it away for 6+ months without touching it

- Want guaranteed returns — CDs offer fixed rates, so you know exactly how much you'll earn

- Are saving for a specific goal — Wedding, vacation, down payment with a known timeline

Try Our Free CD Calculator

Calculate your exact CD earnings with different rates, terms, and compounding frequencies.

CD CalculatorBest CD Rates in 2026

| Term | Top Rate | Average Rate | Best For |

|---|---|---|---|

| 3 months | 4.75% | 4.20% | Emergency fund, short-term savings |

| 6 months | 5.00% | 4.50% | Short-term goals |

| 1 year | 5.10% | 4.75% | Best overall rate |

| 18 months | 4.90% | 4.60% | Medium-term goals |

| 2 years | 4.75% | 4.40% | Goal-based saving |

| 3 years | 4.60% | 4.25% | Longer-term planning |

| 5 years | 4.50% | 4.10% | Maximum yield |

How to Use a CD Calculator

This is how much you plan to invest. Most banks require $500-$1,000 minimum.

Use the annual interest rate (not APY) offered by your bank. Check their website for current rates.

Select how many months you want to lock your money. Longer terms usually mean higher rates.

Most CDs compound monthly. Check with your bank for their specific compounding schedule.

See your maturity value, total interest earned, and APY instantly.

Real-World Examples

Example 1: Short-Term CD

You have $5,000 and won't need it for 6 months.

| Input | Value |

|---|---|

| Deposit | $5,000 |

| Rate | 5.00% |

| Term | 6 months |

| Compounding | Monthly |

| Maturity Value | $5,125.77 |

| Interest Earned | $125.77 |

Example 2: Long-Term CD

You have $25,000 for retirement savings in 3 years.

| Input | Value |

|---|---|

| Deposit | $25,000 |

| Rate | 4.60% |

| Term | 36 months |

| Compounding | Monthly |

| Maturity Value | $28,700.60 |

| Interest Earned | $3,700.60 |

CD Strategies to Maximize Returns

1. CD Ladder

Split your money across CDs with different maturity dates. This gives you regular access to your cash while earning higher rates. For example, with $10,000, you could split it into five $2,000 CDs with terms of 6 months, 1 year, 18 months, 2 years, and 3 years. As each CD matures, you reinvest it at the longest term. Learn more about CD laddering →

2. Barbell Strategy

Put some money in short-term CDs (3-6 months) for liquidity and the rest in long-term CDs (3-5 years) for maximum yield. This approach gives you quick access to some funds while locking in high rates on the rest.

3. Rate Shopping

Online banks typically offer 0.5-1% higher rates than traditional banks. Credit unions may offer even better rates. Always compare rates across multiple institutions before committing. Check Bankrate, NerdWallet, or your bank's website for the latest rates.

4. CD Bullet Strategy

Instead of staggering maturities, buy multiple CDs that all mature at the same time. This is useful when you have a large expense coming up (like a down payment) and want to maximize interest until then.

Common CD Mistakes to Avoid

- Not comparing rates — Online banks often pay 1% more than traditional banks. That's $100 more per year on a $10,000 CD.

- Ignoring early withdrawal penalties — If you might need the money early, choose a no-penalty CD or shorter term.

- Forgetting about auto-renewal — Set a reminder before maturity so you can reinvest at the best available rate instead of accepting whatever the bank offers.

- Putting all eggs in one basket — Spread CDs across different banks to stay within FDIC insurance limits ($250,000 per bank).

- Not considering taxes — CD interest is taxable. Factor this into your returns calculation.

- Choosing too long a term — If you're unsure about your timeline, stick with shorter terms (3-12 months) to avoid penalties.

Tax Considerations

CD interest is taxed as ordinary income at your federal tax rate. If you're in the 22% bracket and earn $500 in CD interest, you'll owe about $110 in federal tax. State taxes may also apply depending on where you live.

Consider holding CDs in a tax-advantaged account (IRA, Roth IRA) to avoid annual tax on interest. This is especially beneficial for higher-rate, longer-term CDs where the tax drag can significantly reduce your effective returns.

Tax Tips for CD Investors

- Use tax-advantaged accounts — Hold CDs in IRAs or Roth IRAs to defer or eliminate taxes on interest

- Consider municipal CDs — Some states offer tax-free CDs for residents

- Track your interest — Banks report interest earned on Form 1099-INT

- Plan withdrawals strategically — If possible, withdraw CDs in years with lower income to reduce tax burden

CD Calculator Tips

When using our CD calculator, keep these tips in mind:

- Enter the interest rate, not APY — Most banks quote the interest rate separately from APY. Use the interest rate for accurate calculations.

- Match the compounding frequency — Check with your bank for their specific compounding schedule. Most CDs compound monthly.

- Consider inflation — A 4.5% CD rate with 3% inflation means your real return is only about 1.5%.

- Compare multiple scenarios — Use the calculator to compare different terms, rates, and amounts to find the best option.

- Factor in taxes — The calculator shows pre-tax earnings. Subtract your tax rate to estimate net returns.

Frequently Asked Questions

What is a CD calculator?

A CD calculator is a free online tool that calculates how much your certificate of deposit will be worth at maturity. It uses the compound interest formula to show your future value, total interest earned, and APY based on your deposit amount, interest rate, term, and compounding frequency.

How is CD interest calculated?

CD interest is calculated using the compound interest formula: FV = P(1 + r/n)^(nt), where P is principal, r is annual interest rate, n is compounding frequency, and t is time in years. The more frequently interest compounds, the more you earn.

What is a good CD rate in 2026?

In 2026, top CD rates range from 4.5% to 5.1% APY depending on term length. 1-year CDs typically offer the best rates around 5.0-5.1%, while 5-year CDs offer 4.4-4.5%.

Are CDs better than savings accounts?

Yes, CDs typically earn 4-5% APY while savings accounts earn 0.4-0.6%. A $10,000 CD earns $450-500 per year vs $40-60 in savings. The tradeoff is CDs lock your money for a fixed term.

How does compounding frequency affect CD returns?

More frequent compounding means more interest earned. Daily compounding earns slightly more than monthly, which earns more than quarterly. For a $10,000 CD at 4.5%, the difference between daily and annual compounding is about $10 per year.

What happens if I withdraw from a CD early?

Most banks charge an early withdrawal penalty of 3-6 months of interest for shorter terms and up to 12 months for longer terms. This penalty can reduce your principal, so CDs are best for money you won't need until maturity.

Data Sources

- Bankrate – Best CD Rates (2026)

- NerdWallet – Best CD Rates (2026)

- FDIC – Deposit Insurance FAQs (2026)

- Investopedia – Certificate of Deposit Guide (2026)